It might seem puzzling that the Prime Minister is asking people to conserve foreign exchange, whereas the RBI Governor, the Finance Minister, the Informal Group of Ministers, sundry economists and the media have been reassuring the public, day after day, that the country has ample foreign exchange reserves. Paying no heed to this flood of assurances from the powers that be, both the rupee and share prices fell sharply the day after the Prime Minister’s speech.

The foreign exchange market and the share market know what officialdom and the media prefer not to mention: that India’s foreign exchange reserves are not the accumulated surpluses from trade, i.e., earned from exporting more goods and services than we import. In fact we consistently run deficits on our current account. Instead, the reserves are made up of liabilities – i.e. they are the sums of money that we owed to other countries/persons abroad. If foreign creditors decide not to roll over debt, and foreign investors decide to withdraw their investments, the foreign exchange reserves will fall. In that sense, they are not really ‘reserves’ at all: they are not a buffer against distress.

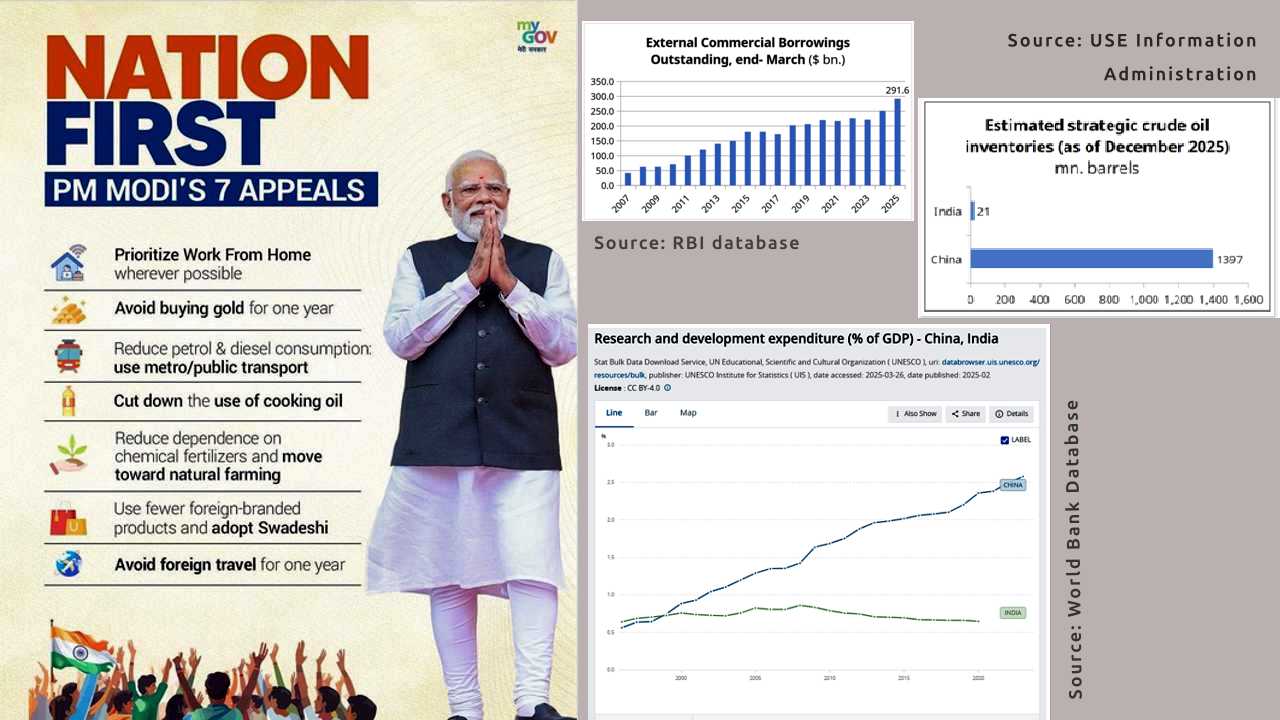

In that sense, the Prime Minister is quite right to raise the alarm. However, his remedy appears to be for the people at large to sacrifice, and lower their standard of living. For example, his appeal to cut down the use of cooking oil is addressed to every household; his appeal to halve the use of chemical fertilisers is addressed to farmers, the single largest section of the country’s workforce.

Such exhortations are unlikely to inspire the desired self-sacrifice, but they lay the ground for imposed sacrifices. The Informal Group of Ministers, while assuring the public of adequate oil, gas and fertiliser supplies, also indicated that the burden of keeping prices at their present level was weighing heavily on the fisc, and may not be sustainable if the international crisis got prolonged.

In other words, the people are being told: prepare to tighten your belts.

But it is not the common people who have created the present foreign exchange crisis.

Who is responsible for the outflow of foreign exchange?

1. It is not the common people that account for the sudden rise in gold imports, which rose by 24 per cent last year, to nearly $72 billion. World Gold Council data for calendar 2025 indicates that 40 per cent of India’s gold imports were accounted for not by jewellery, but by investment demand. That is, wealthy financial investors bought gold to protect their wealth against a fall in the value of the rupee – and indeed furthered the fall of the rupee in the process.¹

2. It is not the common people that send large sums of money out of the country. It is India’s globalised upper classes who have spent over $202 billion in foreign exchange under the Liberalised Remittance Scheme since May 2014, about half on foreign travel and the remainder on other heads. In just the last four years (up to February 2026), they spent $112 billion.

3. The common people of India do not set up ‘family offices’ abroad to manage their global wealth. It is India’s super-rich, people like the Ambanis, that do so. By 2023, the super-rich transferred $130 billion to their family offices in Singapore and $105 billion to those in Hong Kong. (We could not locate a figure for Dubai, another favoured site for this activity.) Some of these funds may be transferred legally.

The super-rich also carry out vast illicit transfers of wealth from India, bringing back sums illicitly when they wish, a process called ‘round-tripping’. Studies have found the sums flowing in and out in this fashion run into the hundreds of billions of dollars, but the powers that be are uninterested in investigating. The sums are staggering: to cite just one type of potential illegal transfer: “orphan imports”, where import payments are made, but no goods were ever despatched, totalled $659 billion over 2000-2018. That is nearly as large as India’s present foreign exchange reserves.

These flows may explain how Indian billionaires manage to accumulate vast funds in offshore tax havens. The Ambanis (not only Anil, but Mukesh), the Adanis, and Agarwal of Vedanta are only a few of the most prominent names. They do not live in fear of being arrested. The much-celebrated digitalisation of India’s tax machinery is being used to hunt the smallest fishes, while giant fishes roam freely. “It will take a long time for us to move ahead in this particular case,” said an official of Mukesh Ambani’s offshore accounts. Mr Adani has emerged spotless from regulatory inquiries. Mr Agarwal lives unmolested in London, where his company is headquartered. (Meanwhile the Indian government actively ousts tribals from their forests and hills, to turn these assets over to Mr Agarwal.)

4. It is not the common people of India who have piled up $292 billion of external commercial borrowings (ECBs). It is the corporate sector which has done so.

Among other things, available foreign borrowings (ECBs) fed the dreams of India’s corporate chieftains in the boom of the 2000s. They went on a vanity shopping spree of companies abroad. Each such loan-backed acquisition added to India’s external debt. Tata Steel made the most outlandish buy, picking up Corus, a U.K.-Dutch firm four times the size of Tata Steel itself, and thereby catapulting themselves into the world’s top 10 steelmakers. The Tatas initially bid $8 billion, but entered a bidding war with another buyer, and finally splurged over $12 billion. The acquisition saddled Tata Steel with foreign loans of $8-9 billion, implying annual interest charges of over $700 million. Corus promptly made steady losses, but the Indian operations of Tata Steel kept generating the cash needed to service its foreign borrowings. Thus India’s natural wealth and surplus flowed to foreign banks.

Among other things, available foreign borrowings (ECBs) fed the dreams of India’s corporate chieftains in the boom of the 2000s. They went on a vanity shopping spree of companies abroad. Each such loan-backed acquisition added to India’s external debt. Tata Steel made the most outlandish buy, picking up Corus, a U.K.-Dutch firm four times the size of Tata Steel itself, and thereby catapulting themselves into the world’s top 10 steelmakers. The Tatas initially bid $8 billion, but entered a bidding war with another buyer, and finally splurged over $12 billion. The acquisition saddled Tata Steel with foreign loans of $8-9 billion, implying annual interest charges of over $700 million. Corus promptly made steady losses, but the Indian operations of Tata Steel kept generating the cash needed to service its foreign borrowings. Thus India’s natural wealth and surplus flowed to foreign banks.

(As an aside, one might ask where, in these times of foreign exchange stringency, Mukesh Ambani plans to obtain the $300 billion he has promised Trump he will invest in a refinery in Texas – a deal Trump calls “THE BIGGEST IN U.S. HISTORY”.)

5. The corporate sector might try to justify these borrowings by saying they are necessary for importing capital goods and making Indian industry more efficient. However, in this entire period, the trade deficit of India’s manufacturing sector has continued to balloon.

Even as it has raked in handsome profits, Indian industry has failed to invest in research and development (R&D), and has preferred to go in for repetitive technology imports, all paid for in hard currency. India’s R&D expenditure is a meagre 0.6-0.7 per cent of GDP; indeed it has been falling since 2010. Within this meagre spending on innovation, only 36 per cent is in the private sector – the rest is in Government labs. It is telling that the private corporate sector’s R&D spending is about half of what India pays out at present on royalties to foreign firms.

Thus India’s celebrated ‘telecom revolution’, near-universal coverage of mobile telephony, has come and gone, without India’s private corporate sector making anything – neither the equipment nor the software nor even the mobile devices. India’s software giants, TCS, Infosys, and the rest have raked in profits at a hectic pace over the years, but actually shrunk their capital expenditure as a share of their cash from operations. Little wonder that they are now facing a question of their existence.

Thus India’s celebrated ‘telecom revolution’, near-universal coverage of mobile telephony, has come and gone, without India’s private corporate sector making anything – neither the equipment nor the software nor even the mobile devices. India’s software giants, TCS, Infosys, and the rest have raked in profits at a hectic pace over the years, but actually shrunk their capital expenditure as a share of their cash from operations. Little wonder that they are now facing a question of their existence.

So it is India’s special class of corporate chieftains who have rendered India permanent dependent, causing it to bleed trade deficits indefinitely. This dependent corporate class drains foreign exchange, and indeed the surplus, from India.

6. Fundamentally, over decades of neoliberal policy, India has been increasingly exposed to flows of international speculative capital. Foreign portfolio investment (FPI) in India’s share market is particularly volatile, but foreign direct investment (FDI) too now consists mainly of speculative financial investments by private equity firms and the like, routed through places such as Singapore and Mauritius. India’s outward FDI too goes to such tax havens. As India’s economy enters more turbulent times, FPI investors are pulling out their money, and FDI net inflows have plummeted. In recent years the Government also opened up government bonds for foreign investors; these investors too are now exiting, and the Government is contemplating giving them tax concessions to lure them back.

All this underlines the fact that capital account liberalisation, i.e., the opening up of the economy to unrestricted capital inflows and outflows, has rendered India more vulnerable. It is thus State policy which is responsible for the present situation: Not the Iran war, nor the consumption needs of India’s common people.

Who is responsible for the shortage of essential commodities?

7. India’s kisans are now told to halve their fertiliser use, as if it were like taking less sugar in one’s tea. This exhortation subtly implies that the kisans are responsible for India’s fertiliser crisis, by their wasteful application. In fact it is the Indian rulers, of both Congress and BJP varieties, that are entirely responsible for the crisis. By 2000, India was self-sufficient at least in urea (on a predominantly public sector base). Thereafter, successive neoliberal governments stopped public investment, even closing down several public sector plants. The private corporate sector made meagre investments. Although the BJP government eventually decided to revive five public sector fertiliser plants, even this was too little to ward off the shortage and import dependence we see today.² India is staring at possible shortfalls just as sowing operations are about to start

India’s rulers received ample warnings from three recent international shocks. The first was during Covid, when urea prices tripled. The second was when fertiliser prices again soared with the Ukraine war. In these years, shortages of fertiliser in various regions resulted at times in riots as well as peasant suicides. Finally, in June 2025, when the US and Israel attacked Iran, it was clear that the Hormuz Strait might at some point be closed, blocking shipments of fertiliser as well as LNG (a feedstock for fertiliser). All these warnings were ignored by the Indian authorities.

So kisans are told today to simply make do with less. In fact, since 50-55 per cent of the present yield of foodgrains is attributed to the addition of chemical fertilisers, any such drastic step would simply lead to a fall in output.³

8. India’s common people are instructed to eat less edible oil, in the cause of saving the country foreign exchange. But the people are certainly not responsible for the country’s gigantic dependence on imports of edible oils. India’s peasantry had made the country self-sufficient in edible oilseeds in the 1990s, with help from the National Mission on Oilseeds of 1986. However, with India’s entry into the WTO, the protection for domestic oilseeds was dismantled, and Indian growers could not compete with cheap palm oil imports. Thus India, a country of 1.4 billion, is now the world’s largest importer of edible oil, and depends on imports for 56 per cent of its consumption! Successive Indian governments have failed to promote domestic production of oilseeds with a procurement policy. This critical part of people’s diet is left to the vagaries of international trade and our supplies of foreign exchange.

9. The common people of India, who are asked now to minimise their use of petrol and diesel, may well wonder whether the Government had made any plans for the present contingency. The contrast with China is striking.

However, the Indian government cannot take all the blame for its petroleum policy, since it does not formulate that policy. That job has been left entirely to the US government. After Trump, in his first term, demanded India stop buying Iranian or Venezuelan oil, India promptly obeyed in May 2019. In his second term, Trump demanded India end all imports of Russian oil (which India got at a discount), failing which he would add an extra 25 per cent tariff on top of his existing 25 per cent. India duly started to cut its Russian oil imports. After the US kidnapped the Venezuelan president, and got control of Venezuelan oil, Trump pushed India to buy it. India started importing Venezuelan oil.

However, the Indian government cannot take all the blame for its petroleum policy, since it does not formulate that policy. That job has been left entirely to the US government. After Trump, in his first term, demanded India stop buying Iranian or Venezuelan oil, India promptly obeyed in May 2019. In his second term, Trump demanded India end all imports of Russian oil (which India got at a discount), failing which he would add an extra 25 per cent tariff on top of his existing 25 per cent. India duly started to cut its Russian oil imports. After the US kidnapped the Venezuelan president, and got control of Venezuelan oil, Trump pushed India to buy it. India started importing Venezuelan oil.

The US gave India a temporary waiver for Russian oil when the war with Iran started, and India once again began buying it, but when that waiver expires, it may have to stop again. Despite India’s being in desperate need of liquefied natural gas (LNG), and despite Russia’s offering to provide it on a long-term basis, India has declined Russia’s offer.⁴ Instead the US is compelling India to buy US LNG at exorbitant prices.

As the Indian government has discarded even the fig leaf of sovereignty over its own oil policy, all that remains for it is to exhort its citizens to use less petroleum products (including fertilisers), and preferably stay at home.

10. As mentioned earlier, the Informal Group of Ministers, in its press release of May 11, hinted that the present price levels could not be borne by the Government if the war got prolonged. After all, they pleaded, India’s oil marketing companies have absorbed losses of close to Rs 1,000 crore a day, so that “the burden of global astronomical prices is not passed on to the Indian citizens.” The Finance Ministry more frankly says that “Pass-through of higher import prices to end-users will also moderate demand growth, and, with it, the pressure on the current account [i.e., the broadest measure of trade deficit].”⁵

This ignores the fact that the Centre alone rakes in Rs 3.5 lakh crore in taxes on crude oil and petroleum products in a year, and it raked in over Rs 19 lakh in the five years ending 2024-25. This is an extremely regressive tax, extracted from all the citizens of India, even the poorest of the poor. Why can the Centre not now protect the people from a price hike?

While the Government prepares to tighten the belts of the people, it is worth remembering how it loosened the belts of the corporate sector in 2019, by handing it a giant cut in direct taxes. The share of corporate tax revenue in gross tax revenues of the central government fell from 32 per cent in 2019 to 25 per cent in 2025. A parliamentary committee estimated the revenue loss in just the first two years after the cut at Rs 1.84 lakh crore. The loss would have risen thereafter, as corporate profits rose further.

The supposed purpose of driving India’s corporate tax rates to among the lowest in the world was to spur investment; but in fact, as India’s chief economic advisor recently remarked, “Corporates and the second or third generation entrepreneurs chose to accumulate those cash profits and probably set up family offices elsewhere [i.e., business families’ offshore wealth management firms] rather than investing in real assets on the ground.”⁶ As the big bourgeoisie have made off with lakhs of crores, India’s common people are being asked to tighten their belts yet further. The recent eruption of working class protests indicates they may not be willing to do so.

(Reproduced from https://rupeindia.wordpress.com/2026/05/15/whose-belts-will-be-tightened/)

- The common people do purchase gold out of traditional compulsions, including for dowries, but in fact they bought less gold in 2025 – they simply paid a higher price for it.

- It is true that some level of imports is required as India has no domestic source of potash. The point is that the dependence today is much greater than it need be.

- No doubt there is a case for reducing unbalanced and unscientific use of urea at many places, as well as introducing organic manures and bio-fertilisers. However, any blanket advice may cause grave harm, as soil conditions vary greatly and proper testing is required – for which a major public sector effort is essential.

- Russia has also reportedly offered to supply India fertilisers such as potash, phosphorus and urea. These too, however, would have to cleared by Washington.

- Department of Economic Affairs, Monthly Economic Review, March 2026. Emphasis added.︎

- T.C.A. Sharad Raghavan, “After govt. pulls up private firms on investment, CII says capex grew 67% in September 2025”, The Hindu, May 11, 2026.︎